Do you have any questions? Speak to an RBC licensed insurance advisor, call 1-800-769-2568. We’ll help you get it.

Do you have any questions? Speak to an RBC licensed insurance advisor, call 1-800-769-2568. We’ll help you get it.

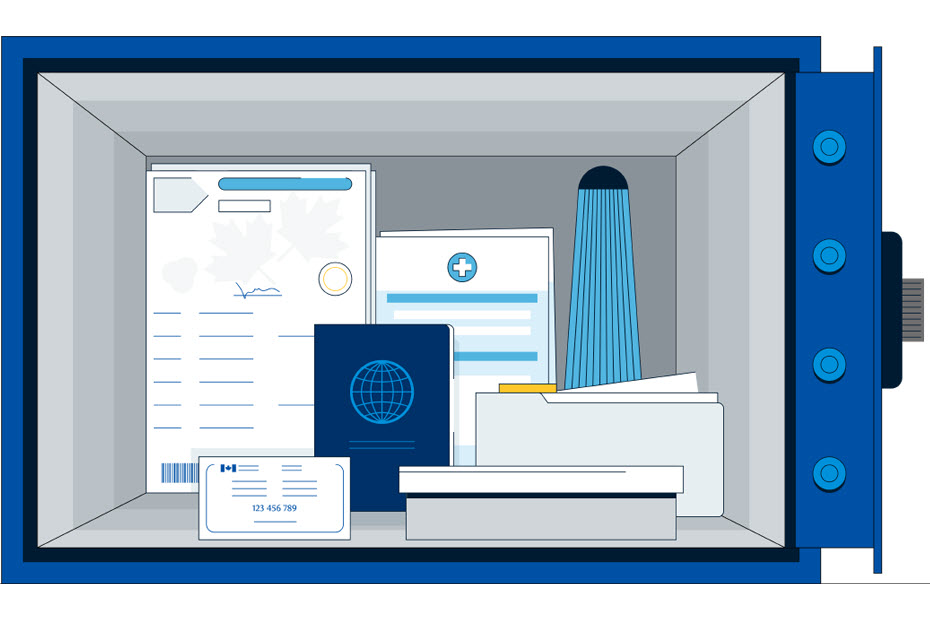

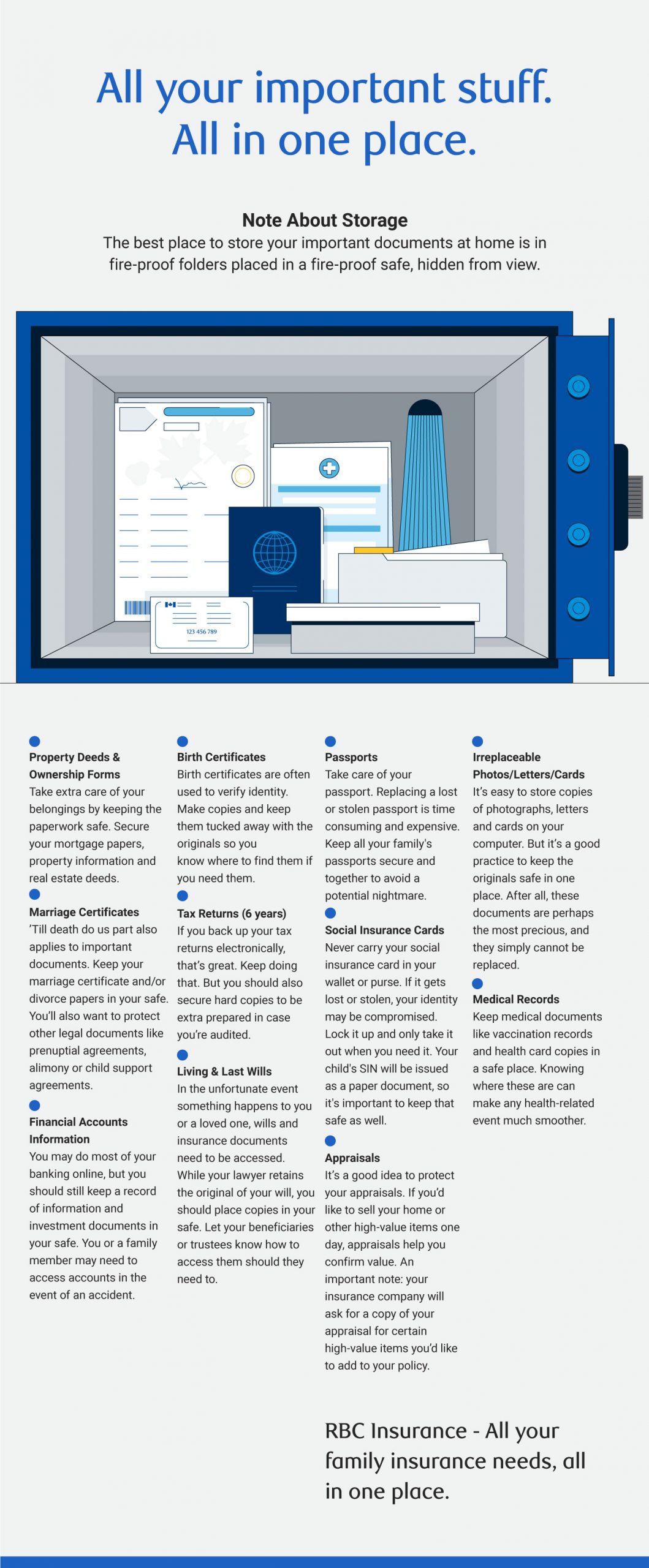

All your important stuff. All in one place.

Note About Storage

- The best place to store your important documents at home is in fire-proof folders placed in a fire-proof safe, hidden from view.

Property Deeds & Ownership Forms

-

- Take extra care of your belongings by keeping the paperwork safe. Secure your mortgage papers, property information and real estate deeds.

Marriage Certificates

-

-

- “Till death do us part” also applies to important documents. Keep your marriage certificate and/or divorce papers in your safe. You’ll also want to protect other legal documents like prenuptial agreements, alimony or child support agreements.

-

Financial Accounts Information

-

-

- You may do most of your banking online, but you should still keep a record of information and investment documents

in your safe. You or a family member may need to access accounts in the event of an accident.

- You may do most of your banking online, but you should still keep a record of information and investment documents

-

Birth Certificates

-

-

- Birth certificates are often used to verify identity. Make copies and keep them tucked away with the originals so you

know where to find them if you need them.

- Birth certificates are often used to verify identity. Make copies and keep them tucked away with the originals so you

-

Tax Returns (6 years)

-

-

- If you back up your tax returns electronically, that’s great. Keep doing that. But you should also secure hard

copies to be extra prepared in case you’re audited.

- If you back up your tax returns electronically, that’s great. Keep doing that. But you should also secure hard

-

Living and Last Wills

-

-

- In the unfortunate event something happens to you or a loved one, wills and insurance documents need to be accessed. While your lawyer retains the original of your will, you should place copies in your safe. Let your beneficiaries or trustees know how to access them should they need to.

-

Passports

-

-

- Take care of your passport. Replacing a lost or stolen passport is time consuming and expensive. Keep all your

family’s passports secure and together to avoid a potential nightmare.

- Take care of your passport. Replacing a lost or stolen passport is time consuming and expensive. Keep all your

-

Social Insurance Cards

-

-

- Never carry your social insurance card in your wallet or purse. If it gets lost or stolen, your identity may be compromised. Lock it up and only take it out when you need it. Your child’s SIN will be issued as a paper document, so it’s important to keep that safe as well.

-

Appraisals

-

-

- It’s a good idea to protect your appraisals. If you’d like to sell your home or other high-value items one day, appraisals help you confirm value. An important note: your insurance company will ask for a copy of your appraisal for certain high-value items you’d like to add to your policy.

-

Irreplaceable Photos/Letters/Cards

-

-

- It’s easy to store copies of photographs, letters and cards on your computer. But it’s a good practice to keep the originals safe in one place. After all, these documents are perhaps the most precious, and they simply cannot be replaced.

-

Medical Records

-

-

- Keep medical documents like vaccination records and health card copies in a safe place. Knowing where these are can make any health-related event much smoother.

-

RBC Insurance — All your family insurance needs, all in one place.

Great Rates and Expert Advice on Home Insurance

Get a free online quote* for coverage to protect you, your property, and your belongings from the unexpected.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Share This Article

Read This Next