Water Damage Insurance in Canada: A Guide for Homeowners

A heavy rainstorm. A frozen pipe in the dead of winter. A washing machine that suddenly overflows. Water has a way of getting into places it shouldn’t in the home — and when it does, the damage can add up quickly.

Over 30 per cent of property damage claims are caused by water, making it the leading cause of home insurance payouts. There’s also potential that number could rise due to 1.5 million households – that’s 10% of all households in Canada – are at high risk for potential flooding. Compounding the problem is Canada’s aging infrastructure where a quarter of the country’s water mains are in need of repair.

As extreme weather becomes more common and municipal infrastructure ages, understanding how insurance coverage for water damage works has never been more important. Here’s what homeowners need to know about what kinds of water damage is covered by home insurance, what’s excluded, and optional coverage available to ensure you have peace of mind.

Key takeaways

- Water damage is a leading cause of home insurance claims in Canada.

- Insurance is designed for unexpected events, not gradual damage or maintenance issues.

- Most standard home insurance policies cover sudden and accidental water damage that originates inside your home, such as a burst pipe or an overflowing appliance.

- Flooding from outside your home, sewer backups, and rising groundwater are typically covered under optional add-on coverage.

- Even diligent homeowners are vulnerable to extreme weather and aging infrastructure, which is why investing in preventative measures is important in protecting your home.

- Because water risks vary by location, season, and property type, reviewing your policy can help ensure you have the right protection in place.

Understanding the risks of water damage

Most water damage in the home comes from one of two sources: internal problems, such as burst pipes or leaky appliances, or external events, such as heavy rain, flash floods, or melting snow.

Water damage risks can also vary by season. Spring snowmelt and heavy rainfall can overwhelm municipal systems, while winter cold snaps increase the risk of frozen pipes. Where you live also matters. In urban areas, aging sewer infrastructure increases the likelihood of backups. Finally, the style of home plays a role. Apartment dwellers, for instance, usually don’t worry about groundwater seepage. However, homeowners with finished basements need to consider the potential effects of seepage, as well as flooding and sewer backup.

No matter the source, the financial impact of water damage can be significant. For example, the average cost of a basement flood is $43,000. Water damage can take an emotional toll, too. Seeing your beloved home and belongings damaged, perhaps destroyed forever, is heartbreaking. There’s also the worry that comes with damage from mold and mildew, as well as the disruption from major repair work.

Read more: How to safely store important documents at home.

What is water damage insurance in Canada?

Water damage insurance is part of your home insurance policy. It helps cover your costs if something unexpected happens from water damage in your property. Most standard home insurance policies include coverage for sudden and accidental internal water escape.

However, not all types of water damage is covered under a basic home insurance policy, so it’s important to know what is and isn’t included. For instance, protection against risks such as sewer backups, sump pump failures, and overland flooding typically requires additional optional policies. The right coverage for water damage depends on your home and where you live as not every location in Canada is eligible for some endorcements. Speak to your insurance provider to learn more.

Standard (included) coverage:

Standard comprehensive policies generally cover sudden and accidental internal water escape, including:

- Burst pipes

- Appliance malfunctions

- Water main damage

Keep in mind, insurance usually covers the damage water causes—like ruined floors, drywall, or your belongings—but not the cost to fix or replace the broken pipe or appliance itself.

Optional (add-on) coverage:

Optional endorsements increase protection for your property to include external factors, including:

- Sewer backup

- Overland water (flood)

- Service line coverage

What forms of water damage does insurance cover?

Leaks and burst pipes are among the most common reasons Canadians file water damage claims, but water can cause trouble in many ways. Most home insurance covers sudden and accidental water damage, including:

Internal systems and plumbing

This means damage to the pipes and water systems that keep your home running smoothly, including:

- Burst or frozen pipes: Coverage usually applies to sudden ruptures in plumbing, heating, or air conditioning systems.

- Plumbing failures: Includes accidental escape of water or steam from indoor plumbing, fixtures, or sprinkler systems.

Household appliances and containers

Standard policies often cover unexpected “indoor floods” caused by everyday household items, including:

- Malfunctioning appliances: Overflows or sudden leaks from appliances such as washing machines, dishwashers, and refrigerators are typically covered.

- Domestic water containers: Accidental overflows from hot water tanks, bathtubs, sinks, and toilets are generally included.

Exterior infrastructure and storm damage

Some types of exterior water damage require additional coverage, but a basic policy usually covers the following:

- Public infrastructure: Damage caused by a break in a municipal water main is commonly covered.

- Storm-caused openings: If wind or hail suddenly breaks a window or makes a hole in your roof, insurance usually covers the water damage that gets inside.

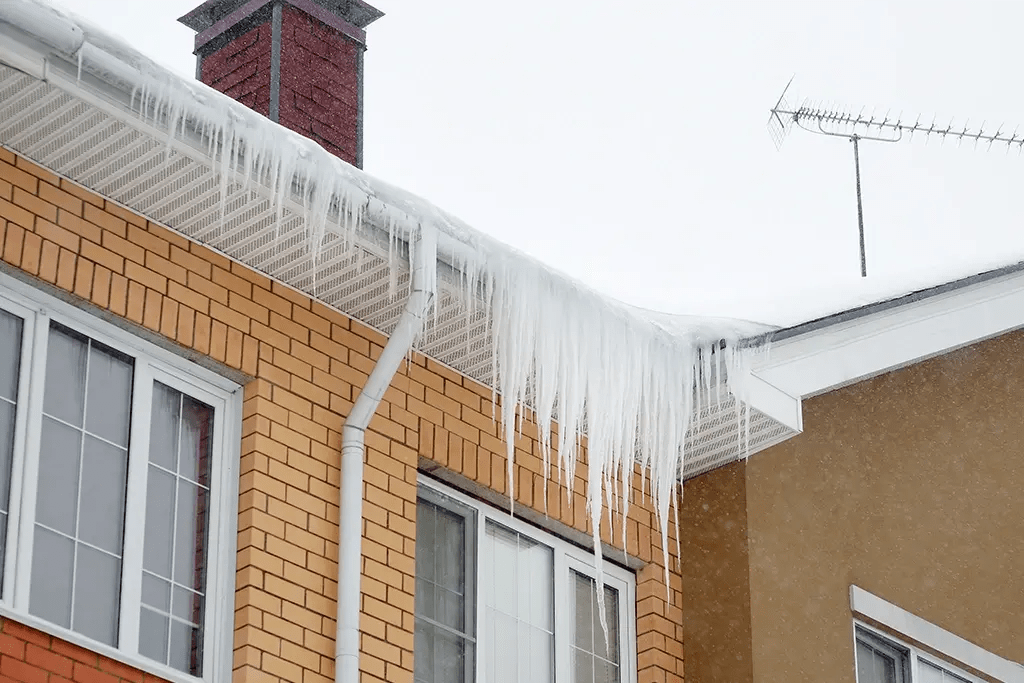

- Ice damming and roof leaks: Many policies cover damage from ice dams that push melting water under your shingles, and leaks through eavestroughs or downspouts.

Read more: What homeowners need to know about ice damming.

What forms of water damage does insurance not cover?

Not all water damage to property is covered by insurance. These are important exclusions to consider:

Gradual damage and lack of maintenance

Home insurance is there for sudden problems, not ongoing maintenance. Slow leaks, repeated seepage, or pipes that freeze when the heat is turned off are typically not covered. If outdoor containers or appliances freeze because you didn’t take precautions, that’s often not covered either.

Overland floods and sewer backups

Basic home insurance usually doesn’t cover flooding from outside (including when the snow melts in spring) rising groundwater, or sewer backups. You’ll need to add extra coverage for these risks.

Groundwater seepage

If water slowly seeps in through your foundation, basement floor, or window wells, it’s typically considered a maintenance issue. However, you can purchase coverage for sudden and accidental groundwater entry to cover you from groundwater entry.

Unoccupied homes

If your home is empty for more than 30 days in a row, most water damage coverage stops. Empty homes are riskier because a small leak can turn into a big problem before anyone notices. You’ll usually need special permission or inspections to keep your coverage. If your home is considered vacant and your home insurer has agreed to continue coverage, water damage coverage is usually not covered.

Coastal flooding and storm surges

Even with extra coverage, most Canadian home insurance won’t cover damage from ocean water, like tidal waves, tsunamis, or storm surges. Damage from spray, ice, or debris from these events is also usually excluded.

Types of water damage coverage in Canada

Accidental or sudden water damage coverage

This is the basic coverage in most Canadian home insurance policies. It covers sudden or accidental water problems inside your home, such as burst pipes, leaky dishwashers, or plumbing failures. It covers the damage to your walls, floors, and belongings, but not the cost of fixing or replacing the broken pipe or appliance. You’ll still need to pay your deductible, and coverage has limits.

Sewer backup coverage

This extra property coverage protects you if wastewater comes into your home through floor drains, toilets, or sinks. Overloaded city systems or dysfunctional sump pumps are often to blame. Since basic insurance doesn’t cover sewage coming in from outside, this add-on is the main way to protect yourself from one of the most expensive and stressful types of water damage. It’s especially important if you have a finished basement or live in an area with older pipes.

Overland water coverage

Overland water coverage protects you from flooding that starts at ground level—like heavy rain, fast snowmelt, or overflowing rivers and lakes. With severe weather becoming more common, this coverage is a smart choice if you live in a low-lying area or in an area that floods in the spring. It’s often bundled with sewer backup coverage, since both can happen during big storms.

Groundwater coverage

Some insurers offer this extra coverage for damage caused by water rising from underground sources through your foundation, basement walls, or floors. It’s different from overland flood insurance because it covers water coming up from below, not flowing in from outside. This coverage is usually just for sudden problems, not long-term foundation issues or missed maintenance. It’s important to note, not all insurance companies offer this type of coverage, so check with your provider to confirm.

Protect your home from water damage

Regular maintenance can help lower your risk of water damage. On the inside of your home, checking your plumbing, maintaining your appliances, and installing smart leak detectors are all good preventative measures. You should also consider installing a backwater valve to reduce sewer backup risk and test your sump pump annually.

On the outside, ensure proper grading around your foundation, clean eavestroughs and downspouts regularly, and insulate exposed pipes in colder months. If you’re away, arrange for someone to check in on your home regularly.

Knowing what your home insurance policy covers is the best way to avoid unexpected costs. Review the details, such as coverage for sewer back up and overland flood, and confirm your deductible amounts as there is sometimes a different deductible for water claims. Finally, don’t forget to update your coverage after significant renovations. Updating your coverage doesn’t always mean an increase in your premiums, but will ensure you have the right coverage in the event of a claim.

Have questions? Talk to your insurance representative to discuss your home insurance options and water damage coverage to protect your home and your personal property.

FAQs about water damage insurance for homeowners

Does home insurance cover water damage in Canada?

Most standard home insurance policies cover what’s known as sudden and accidental internal water damage. That includes things such as from a burst pipe or defective appliance. Coverage for external threats—such as sewer backups, rising groundwater, or overland flooding—typically requires add-on coverage.

Is sewer backup covered by home insurance?

Sewer backup coverage is not automatically included in most standard policies. It is available as an optional add-on and is strongly recommended for homeowners.

Do I need overland water insurance in Canada?

It depends on where you live — but for many Canadians, the answer is increasingly yes. Flood damage is on the rise in Canada and overland water insurance is increasingly important. This is especially true for homeowners in low-lying areas or districts prone to heavy rainfall and rapid snowmelt.

Are frozen pipes covered by home insurance?

Generally speaking, yes. Damage from frozen pipes is usually covered if it happens unexpectedly and you’ve taken reasonable precautions. However, if your home was left unheated or unattended for an extended period without reasonable precautions, your claim may be denied.

My basement flooded, will I be covered?

Your insurance coverage depends on the source of the water and the specifics of your policy. A flood caused by a burst internal pipe is typically covered under a standard policy. However, if water entered through your foundation or backed up through a drain, coverage generally only applies if you have added overland water, or sewer backup protection.

Great Rates and Expert Advice on Home Insurance

Get a free online quote* for coverage to protect you, your property, and your belongings from the unexpected.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.